Software program shares, lengthy seen as among the market’s most engaging enterprise fashions, have been hit laborious in latest months as investor considerations round synthetic intelligence and huge language fashions intensified. The selloff has been vital, with the iShares Expanded Tech-Software program Sector ETF (IGV), a broadly adopted proxy for the software program house, falling greater than 20% over that stretch. The concern is that AI will materially disrupt conventional software program economics. Whereas that threat is actual, expectations seem to have moved too far, too quick. AI is prone to reshape elements of the software program panorama, however it’s unlikely to render whole classes out of date.

Consequently, the market seems to be pricing in a stage of disruption that doesn’t align with the sturdiness of the strongest platforms. Over time, sentiment tends to imply revert, and that dynamic is now creating compelling alternatives amongst premium software program names.

Picture Supply: TradingView

For a lot of the previous decade, Wall Road assigned substantial valuation premiums to software program firms, attracted by asset mild fashions, excessive margins, recurring income, and near-zero marginal prices. For my part, a lot of these premiums turned extreme, bordering on structural overvaluation, which stored me cautious on the sector regardless of the standard of the companies. That backdrop has modified meaningfully.

At present, a number of of the {industry}’s strongest franchises are buying and selling close to cyclical lows, at the same time as their aggressive positions stay intact. AppLovin (APP), Palantir Applied sciences (PLTR), Salesforce (CRM), ServiceNow (NOW), and Robinhood Markets (HOOD) stand out as main platforms the place valuations have reset and risk-reward profiles have gotten more and more tough to disregard.

Picture Supply: Zacks Funding Analysis

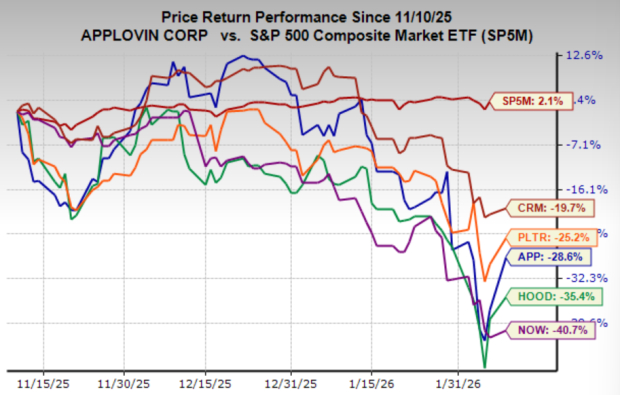

AppLovin: Inventory Rebound Might Sign the Begin of the Subsequent Leg Larger

AppLovin shares are surging immediately after latest cash laundering allegations towards the corporate have been withdrawn, eradicating a key overhang that had pressured the inventory. Previous to the rebound, APP had fallen roughly 50% from its report highs, a drawdown that appeared disconnected from the corporate’s underlying momentum. Whereas the restoration has been sharp, it could symbolize the early phases of a broader transfer greater relatively than a short-lived bounce.

AppLovin has quietly developed into one of many market’s extra compelling progress tales. The corporate has delivered substantial appreciation lately as its industry-leading digital promoting platform expands at a fast tempo. Simply as vital, administration has been aggressive in embedding AI throughout its ecosystem to enhance focusing on, optimize advert efficiency, and drive working leverage, initiatives which are more and more flowing by way of to the underside line.

The corporate presently carries a Zacks Rank #2 (Purchase), supported by modest upward revisions to earnings estimates. Gross sales are projected to climb 18.2% this 12 months and speed up one other 38.3% subsequent 12 months, whereas earnings are anticipated to surge 106% adopted by a further 62.5% acquire. Regardless of that progress profile, the inventory trades at roughly 25x ahead earnings—a a number of that seems affordable given the corporate’s growth charge and enhancing profitability trajectory.

Picture Supply: Zacks Funding Analysis

Salesforce: Shares Commerce at Historic Low cost

Salesforce, one of many authentic SaaS pioneers and a dominant drive in enterprise software program, has additionally been pulled decrease by the prevailing “AI-disrupts-software” narrative. That selloff has occurred regardless of the corporate’s scale, entrenched buyer base, and ongoing innovation. At present, Salesforce carries a Zacks Rank #2 (Purchase), supported by strong progress expectations and a valuation that stands out relative to its personal historical past.

Shares are presently buying and selling at roughly 14.7x ahead earnings, the bottom a number of Salesforce has commanded since turning into a public firm. Income is predicted to develop 9.5% this 12 months and 10.9% subsequent 12 months, whereas earnings are projected to rise 15.3% this 12 months and one other 10.5% subsequent 12 months—respectable progress for a corporation of its measurement.

With increasing AI and huge language mannequin initiatives, deep integration throughout enterprise workflows, and constantly robust fundamentals, Salesforce seems mispriced at present ranges and isn’t a inventory buyers ought to overlook.

Palantir Applied sciences: A Market Main Inventory on Sale

Palantir Applied sciences has rapidly established itself as one of many world’s main software program firms, with its share worth reflecting that ascent over the previous a number of years. Supported by deep, long-duration authorities contracts and a set of extremely differentiated information and analytics platforms, Palantir has emerged as one of many market’s premier software program franchises.

Shares have corrected almost 40% over the previous few months as investor sentiment towards AI and software program shifted. That pullback has helped reasonable valuation, although Palantir nonetheless trades at a premium relative to most friends. The inventory presently adjustments arms at roughly 100x ahead earnings, a lofty a number of, however one backed by distinctive progress expectations and a aggressive moat that continues to be largely uncontested.

Income is projected to climb 61.4% this 12 months and 40.8% subsequent 12 months, whereas earnings are anticipated to surge 78.7% this 12 months adopted by a 42.2% enhance subsequent 12 months. Palantir additionally carries a Zacks Rank #2 (Purchase), reflecting continued confidence within the firm’s earnings trajectory regardless of the latest volatility. Earnings estimates have jumped greater than 30% throughout timeframes within the final week alone.

Picture Supply: Zacks Funding Analysis

ServiceNow: SaaS Inventory at a Uncommon Low cost

ServiceNow has lengthy been seen as one of many highest-quality franchises in enterprise software program, often commanding a premium a number of reflective of its sturdy progress and mission vital choices. That dynamic has shifted. Following the broader software program selloff, shares are actually buying and selling at one of the crucial enticing valuations within the firm’s historical past.

Finest recognized for its market main, cloud-based workflow platform, ServiceNow is deeply embedded throughout massive enterprises, serving roughly 85% of the Fortune 500 and about 60% of the World 2000. That stage of penetration underscores each the stickiness of its merchandise and the strategic significance of its software program inside fashionable company infrastructure.

At present, the inventory trades at roughly 24.5x ahead earnings, an all-time low a number of for the corporate, whereas earnings are projected to develop round 24% yearly over the subsequent three to 5 years. Within the nearer time period, income is predicted to develop 20.1% this 12 months and one other 18.2% subsequent 12 months. With shares sitting almost 60% under prior highs, ServiceNow’s mixture of scale, visibility, and sustained progress makes the present setup notably compelling for long-term buyers.

Picture Supply: TradingView

Robinhood Markets: Inventory Momentum Constructing

Robinhood Markets is usually seen much less as a standard software program firm and extra as a fintech platform, however it has quietly developed into one of many market’s extra compelling digital monetary companies. Shares are rebounding as buyers rotate again into former progress leaders, but the inventory nonetheless seems attractively positioned relative to its longer-term fundamentals.

Robinhood has remodeled from an entry-level brokerage right into a multi-product monetary “tremendous app.” Its platform now spans multi-asset buying and selling, wealth administration, banking companies, bank cards, and extra monetary instruments, considerably increasing each its addressable market and monetization potential.

The inventory presently trades at roughly 33.6x ahead earnings, effectively under its historic median a number of of roughly 50.4x. Over the long run, earnings are projected to develop round 26% yearly. Close to-term progress stays strong, with income anticipated to climb 53% this 12 months and 21.8% subsequent 12 months, whereas earnings are forecast to surge 86% this 12 months adopted by a 21.2% enhance subsequent 12 months.

Ought to Buyers Purchase Shares in PLTR, CRM, APP, HOOD and NOW?

Durations of broad pessimism usually create essentially the most enticing entry factors for high-quality progress shares, and the latest software program correction seems to be a kind of moments. Whereas AI introduces official uncertainty, the market could also be overstating the pace and severity of disruption, notably for {industry} leaders with entrenched platforms, robust stability sheets, and sturdy demand.

Valuations throughout a number of premier franchises have reset to ranges hardly ever seen over the previous decade, enhancing the risk-reward profile for long-term buyers. Though volatility might persist because the software program panorama evolves, selectively accumulating basically robust names in periods of dislocation has traditionally confirmed to be a successful technique. For buyers with a multi-year horizon, these 5 shares stand out as compelling candidates for deeper consideration.

Zacks Names #1 Semiconductor Inventory

This under-the-radar firm makes a speciality of semiconductor merchandise that titans like NVIDIA do not construct. It is uniquely positioned to make the most of the subsequent progress stage of this market. And it is simply starting to enter the highlight, which is strictly the place you wish to be.

With robust earnings progress and an increasing buyer base, it is positioned to feed the rampant demand for Synthetic Intelligence, Machine Studying, and Web of Issues. World semiconductor manufacturing is projected to blow up from $452 billion in 2021 to $971 billion by 2028.

See This Inventory Now for Free >>

Salesforce Inc. (CRM) : Free Inventory Evaluation Report

ServiceNow, Inc. (NOW) : Free Inventory Evaluation Report

AppLovin Company (APP) : Free Inventory Evaluation Report

iShares Expanded Tech-Software program Sector ETF (IGV): ETF Analysis Experiences

Palantir Applied sciences Inc. (PLTR) : Free Inventory Evaluation Report

Robinhood Markets, Inc. (HOOD) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.