Wholesome competitors helps drive innovation and in flip, investor returns.

That’s precisely what we’ve seen between two of the world’s largest chipmakers. The previous yr has been notably noteworthy for Superior Micro Units, which not solely staged a robust restoration however meaningfully outperformed Nvidia, the longtime AI chief.

By way of share returns, AMD shares rose roughly 77% in 2025, practically doubling Nvidia’s extra modest 39% achieve. Whereas the 2 shares moved in tandem through the first half of the yr, the divergence gained steam within the latter half, notably after AMD inked a multi-year deal to energy OpenAI’s next-generation AI infrastructure.

Picture Supply: StockCharts

AMD CEO Lisa Su referred to the partnership as a “true win-win, enabling the world’s most bold AI buildout and advancing your complete AI ecosystem.” The phrases of the deal included deploying 6 gigawatts of AMD GPUs.

As we progress into 2026 with AMD buying and selling round $250 per share in mid-January, the inventory’s story stays compelling. The corporate’s disciplined execution and increasing AI footprint present a honest alternative for these looking for publicity to the continued information middle transformation.

Why AMD’s Outperformance Appears to be like Set to Proceed

AMD’s ascent in 2025 stemmed from a confluence of things that highlighted its evolution from a perennial challenger to a reputable menace in high-performance computing. The info middle phase, now the core development engine, delivered report income all year long. In Q3 2025, this phase posted $4.3 billion in revenues—up 22% year-over-year—pushed by sturdy demand for fifth Gen EPYC processors and Intuition accelerators.

AMD’s MI300 collection ramps exceeded expectations, securing wins with main hyperscalers and enterprises looking for alternate options amid Nvidia provide constraints and pricing pressures. Administration’s steerage for higher than 60% CAGR in information middle income over the subsequent a number of years underscored this momentum, reflecting confidence in product superiority and ecosystem partnerships.

A pivotal second got here with the MI355X accelerator, positioned as a cheap competitor to Nvidia’s choices, gaining traction for its performance-per-dollar benefits. This helped AMD seize incremental share in inference workloads, the place effectivity issues as a lot as uncooked coaching energy.

Shopper and gaming segments additionally contributed, with Ryzen processors benefiting from AI PC refreshes. General, AMD’s whole income development accelerated to the mid-30% vary through the third quarter of final yr, translating into sharp earnings enlargement and a constant pattern of exceeding expectations.

In distinction, Nvidia – whereas nonetheless dominant with explosive development earlier within the cycle – confronted a better bar in 2025. Its shares superior solidly however lagged AMD as traders digested potential saturation in coaching demand, export restrictions impacting China income, and a premium valuation that left much less room for error.

Nvidia’s NVDA quarterly development remained spectacular, however AMD’s relative undervaluation on the time—buying and selling at decrease ahead multiples regardless of comparable AI publicity—drew rotation. AMD’s beneficial properties had been amplified within the yr’s second half, as proof mounted of diversifying buyer bases and open ecosystems decreasing Nvidia lock-in dangers.

This outperformance wasn’t a mere catch-up; it signaled structural shifts. Along with the OpenAI deal, partnerships with Microsoft, Meta, and Oracle for customized deployments supplied validation for AMD shareholders.

Seeking to 2026, there’s little doubt that AMD AMD inventory nonetheless holds enchantment. The AI inferencing market—projected to develop sooner than coaching—is AMD’s candy spot, with MI400 collection accelerators unveiled at CES 2026 promising vital leaps in effectivity and scale. The complete MI400 lineup, together with Helios racks for exascale computing, positions AMD to capitalize on broadening deployments past hyperscalers.

What the Zacks Mannequin Reveals

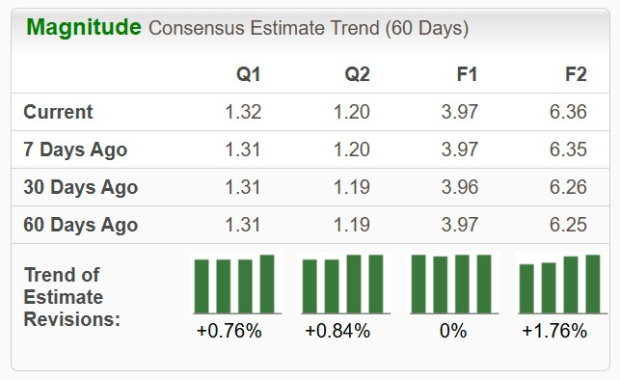

The upcoming This fall 2025 earnings report is about to be launched on February 3rd and must be a key catalyst. Analysts have bumped up EPS estimates by 0.76% previously 60 days. The Zacks Consensus Estimate now stands at $1.32 per share, reflecting a 21.1% enchancment versus the year-ago interval. Revenues are anticipated to leap 26% to $9.65 billion.

Picture Supply: Zacks Funding Analysis

The Zacks Earnings ESP (Anticipated Shock Prediction) indicator seeks to seek out corporations which have lately seen optimistic earnings estimate revision exercise. This newer info has confirmed to be very helpful find optimistic earnings surprises, giving traders a leg up throughout earnings season. In reality, when combining a Zacks Rank #3 or higher and a optimistic Earnings ESP, shares produced a optimistic shock 70% of the time in response to our 10-year backtest.

AMD is at the moment a Zacks Rank #3 (Maintain) inventory and boasts a +2.01% Earnings ESP. One other beat could also be within the playing cards when the corporate reviews its This fall leads to early February.

Backside Line

In reflecting on this dynamic duo, competitors in the end advantages the trade—pushing boundaries in energy effectivity and accessibility.

For traders, AMD presents a balanced approach to take part in AI’s subsequent part. It is a story of perseverance paying off, and one value contemplating thoughtfully.

Radical New Expertise May Hand Buyers Large Good points

Quantum Computing is the subsequent technological revolution, and it may very well be much more superior than AI.

Whereas some believed the expertise was years away, it’s already current and shifting quick. Giant hyperscalers, equivalent to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Cook dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what may very well be “the subsequent huge factor” in quantum computing supremacy. At present, you have got a uncommon likelihood to place your portfolio on the forefront of this chance.

See High Quantum Shares Now >>

Superior Micro Units, Inc. (AMD) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.