Costco Wholesale Company COST inventory has prolonged its current rally after the retailer reported robust December gross sales. As a dominant participant within the warehouse membership area, Costco continues to profit from a resilient membership-driven mannequin, regular site visitors developments and enhancing digital demand. The upbeat gross sales have drawn investor consideration to a key query: Ought to shareholders purchase extra, maintain tight or begin reserving earnings at present ranges?

Costco shares have superior 9.2% because the firm reported its December gross sales outcomes on Jan. 7. Over the previous month, the inventory has risen 13.3%, outpacing the trade‘s achieve of 9.6%. The December report confirmed stable comparable gross sales progress throughout areas and a pointy acceleration in e-commerce, strengthening the narrative that Costco’s operational execution and buyer loyalty stay intact regardless of a difficult retail backdrop.

When put next with its friends, Costco has underperformed Goal Company TGT however fared higher than Ross Shops, Inc. ROST and Greenback Common Company DG. Whereas shares of Goal have risen 16.8%, these of Greenback Common and Ross Shops have jumped 8.1% and 6.4%, respectively.

Picture Supply: Zacks Funding Analysis

Decoding Costco’s December Gross sales Report

Costco’s membership-driven mannequin stays a core power, with excessive renewal charges guaranteeing a reliable income stream. Its environment friendly provide chain and bulk buying energy allow aggressive pricing, reinforcing its robust market place. This mixture of buyer loyalty and operational effectivity continues to provide Costco a bonus in a aggressive retail panorama.

For the 5 weeks ended Jan. 4, 2026, Costco reported a 7% year-over-year enhance in complete comparable gross sales. Regionally, comparable gross sales rose 6% in america, 8.4% in Canada and 10.6% in Different Worldwide markets. Digitally enabled comparable gross sales in December surged 18.9%. (Learn: Costco’s December Gross sales Keep Sturdy: What Is Driving COST’s Momentum?)

In consequence, Costco’s web gross sales for December rose 8.5% to $29.86 billion, up from $27.52 billion in the identical interval final 12 months. This follows a gross sales enchancment of 8.1% and eight.6% in November and October, respectively, reflecting a powerful and constant gross sales efficiency over the previous few months.

A Sneak Peek Into Costco’s Tailwinds

Costco’s fundamental power is its resilient membership-based enterprise mannequin, which acts as a strong progress engine. This setup supplies a gradual and predictable income stream from annual charges, setting Costco aside from conventional retailers. Importantly, the mannequin creates a powerful worth proposition, resulting in persistently excessive membership renewal charges. This method helps Costco’s aggressive benefit, enabling it to function on slim margins whereas attaining excessive gross sales volumes.

The corporate’s operational self-discipline is evident in its meticulous method to supply-chain administration and procurement. By leveraging scale and effectivity, Costco routinely secures favorable phrases with suppliers and passes financial savings on to prospects. This disciplined price administration improves margins and shields the corporate from inflationary pressures.

Costco’s capability to adapt to altering shopper preferences has additionally been key to its progress. The corporate modifies its product combine to incorporate each on a regular basis necessities and distinctive, high-demand gadgets — a method that broadens its enchantment throughout numerous buyer teams. Utilizing data-driven market evaluation and versatile merchandising, Costco has step by step expanded its presence each domestically and internationally.

Costco’s strategic investments in know-how and logistics are strengthening its multi-channel ecosystem. The corporate’s digital initiatives have improved member engagement and operational effectivity, combining on-line comfort with the effectiveness of its warehouse mannequin. The corporate’s same-day supply providing is powered by Instacart, Uber Eats and DoorDash. By boosting e-commerce capabilities and increasing logistics infrastructure, Costco not solely faucets into new progress alternatives but in addition ensures secure demand from a large member base that values reliability and comfort equally.

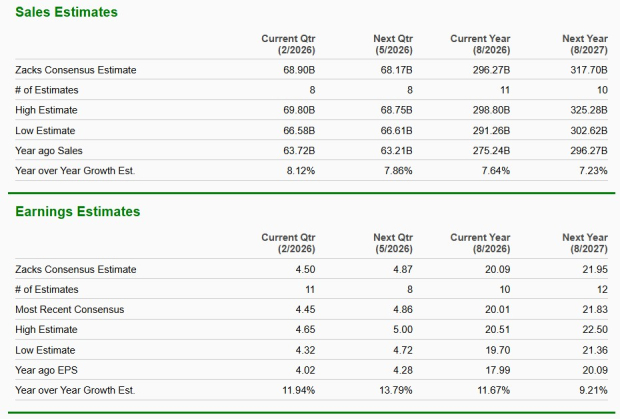

How Consensus Estimates Stack Up for Costco

The Zacks Consensus Estimate for Costco’s present financial-year gross sales and earnings per share implies year-over-year progress of seven.6% and 11.7%, respectively.

Picture Supply: Zacks Funding Analysis

Does Costco’s Valuation Replicate Energy or Stretch?

Costco is buying and selling at a premium to its trade friends. The corporate’s ahead 12-month price-to-earnings ratio stands at 46.31, larger than the trade’s ratio of 31.94 and the S&P 500’s ratio of 23.21. Nevertheless, the inventory is buying and selling under its median P/E stage of 49, noticed over the previous 12 months.

Costco is buying and selling at a premium to Goal (with a ahead 12-month P/E ratio of 14.43), Greenback Common (21.10) and Ross Shops (27.04).

Picture Supply: Zacks Funding Analysis

Now, the query arises whether or not Costco’s present worth is warranted or overvalued in at this time’s market.

The corporate’s excessive valuation reveals that buyers have robust religion within the firm’s regular progress, loyal buyer base and stable enterprise mannequin. This premium could also be deserved, given Costco’s constant efficiency, nevertheless it additionally means the inventory has much less room for error. At this stage, a few of the future progress could already be priced in, making it more durable to justify additional upside.

Easy methods to Play Costco: Purchase, Maintain or Promote?

Costco’s December gross sales outcomes reaffirm its place as a reliable inventory within the retail sector, backed by robust membership progress, constant comparable gross sales enchancment and stable monetary fundamentals. Whereas the inventory trades at a premium valuation, this seems justified, given its operational resilience, increasing world footprint and constant buyer base. For long-term buyers prepared to pay up for high quality and stability, Costco stays a compelling selection. Nevertheless, for value-conscious consumers, the elevated valuation could warrant endurance for a extra engaging entry level. Costco presently carries a Zacks Rank #3 (Maintain). You’ll be able to see the whole checklist of at this time’s Zacks #1 Rank (Sturdy Purchase) shares right here.

#1 Semiconductor Inventory to Purchase (Not NVDA)

The unimaginable demand for information is fueling the market’s subsequent digital gold rush. As information facilities proceed to be constructed and always upgraded, the businesses that present the {hardware} for these behemoths will turn into the NVIDIAs of tomorrow.

One under-the-radar chipmaker is uniquely positioned to benefit from the subsequent progress stage of this market. It focuses on semiconductor merchandise that titans like NVIDIA do not construct. It is simply starting to enter the highlight, which is strictly the place you wish to be.

See This Inventory Now for Free >>

Goal Company (TGT) : Free Inventory Evaluation Report

Greenback Common Company (DG) : Free Inventory Evaluation Report

Costco Wholesale Company (COST) : Free Inventory Evaluation Report

Ross Shops, Inc. (ROST) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.