Capital One COF is scheduled to announce fourth-quarter and 2025 outcomes on Jan. 22, after market shut. Much like the earlier reported quarter, the corporate’s to-be-reported quarter’s efficiency is anticipated to have been pushed by its stable bank card enterprise, together with the acquisition of Uncover Monetary.

The Zacks Consensus Estimate for COF’s fourth-quarter revenues is pegged at $15.32 billion, which signifies year-over-year progress of fifty.3%. The consensus estimate for full-year gross sales of $53.25 billion implies an increase of 36.2% from the earlier yr.

Nevertheless, up to now seven days, the consensus estimate for earnings for the to-be-reported quarter has been revised 2.2% decrease to $3.98. The estimate signifies a 28.8% enchancment from the prior-year quarter’s precise.

For 2025, the consensus estimate for earnings is $19.65, which signifies progress of 40.8%.

Estimate Revision Pattern

Picture Supply: Zacks Funding Analysis

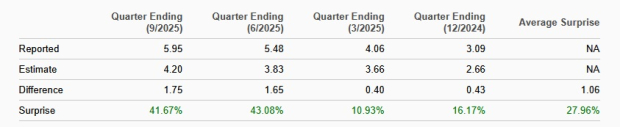

COF has a formidable earnings shock historical past. The corporate’s earnings outpaced the Zacks Consensus Estimate in every of the trailing 4 quarters, the typical beat being 28%.

Earnings Shock Historical past

Picture Supply: Zacks Funding Analysis

Key Elements More likely to Affect Capital One’s This fall Outcomes

NII: Within the to-be-reported quarter, the Federal Reserve lowered rates of interest twice. This, together with the speed lower in September, is more likely to have damage Capital One’s internet curiosity revenue (NII) to some extent.

Nevertheless, the general lending state of affairs was sturdy within the fourth quarter. Per the Federal Reserve’s newest information, the demand for shopper loans was sturdy.

Furthermore, the Zacks Consensus Estimate for complete common incomes belongings for COF is pegged at $587.8 billion, implying a 27.6% rise from the prior-year quarter. Thus, regardless of declining charges, a stable lending state of affairs and stabilizing funding/deposit prices are anticipated to have aided NII.

Additionally, Capital One’s continued efforts to strengthen its card operations are anticipated to have offered assist. The consensus estimate for fourth-quarter NII of $12.25 billion signifies 51.3% year-over-year progress.

Price revenue: Supported by an total rise in bank card utilization and the Uncover Monetary buyout, Capital One’s interchange charges (constituting greater than 60% of payment revenue) are more likely to have elevated within the quarter beneath evaluate. The Zacks Consensus Estimate for interchange charges is $1.88 billion, suggesting a 49.2% year-over-year bounce.

The consensus estimate for service prices and different customer-related charges of $866 million implies 56.3% progress from the prior-year quarter. The Zacks Consensus Estimate for different non-interest revenue is pegged at $313 million, indicating a 12.6% rise.

Thus, the consensus estimate for complete non-interest revenue of $3.03 billion signifies a bounce of 44.6% from the prior-year quarter.

Bills: Capital One has been witnessing a persistent rise in bills over the previous a number of quarters because of increased advertising prices and funding in know-how upgrades. Additional, the Uncover Monetary acquisition, together with inflation stress, is anticipated to have resulted in a rise in working bills within the fourth quarter.

Asset High quality: Capital One is much less more likely to have put aside an enormous sum of money for potential delinquent loans, because the rates of interest have come down considerably from the highs of 5-5.25%.

What Our Quantitative Mannequin Unveils for COF

In keeping with our quantitative mannequin, the possibilities of Capital One beating the Zacks Consensus Estimate for earnings this time are excessive. It is because it has the precise mixture of the 2 key substances — a optimistic Earnings ESP and a Zacks Rank #3 (Maintain) or higher.

You’ll be able to uncover the most effective shares to purchase or promote earlier than they’re reported with our Earnings ESP Filter.

Earnings ESP: The Earnings ESP for Capital One is +2.07%.

Zacks Rank: The corporate at present carries a Zacks Rank #3. You’ll be able to see the whole checklist of at this time’s Zacks #1 Rank (Sturdy Purchase) shares right here.

Capital One’s Value Efficiency & Valuation Evaluation

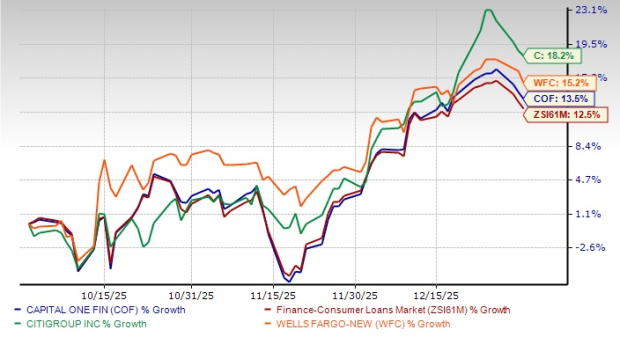

Within the fourth quarter, the COF inventory rallied 13.5%, outperforming the Zacks Client Loans trade. Its friends Wells Fargo WFC and Citigroup C gained 15.2% and 18.2%, respectively.

4Q25 Value Efficiency

Picture Supply: Zacks Funding Analysis

Wells Fargo’s fourth-quarter 2025 adjusted earnings per share of $1.76 surpassed the Zacks Consensus Estimate of $1.66. Within the prior-year quarter, the corporate reported earnings per share of $1.42. Its outcomes benefited from an enchancment in NII, increased non-interest revenue and decrease provisions.

Citigroup’s fourth-quarter 2025 adjusted internet revenue per share of $1.81 elevated 35.1% from the year-ago interval. The metric additionally surpassed the Zacks Consensus Estimate by 9.7%. Outcomes benefited from a rise in NII and decrease provisions. Citigroup additionally registered a year-over-year enhance in funding banking revenues, reflecting progress in Advisory and Fairness Capital Markets.

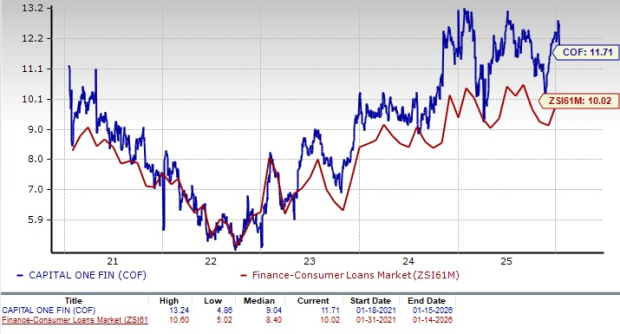

COF shares seem costly relative to the trade. The inventory is, at current, buying and selling at a ahead 12-month value/earnings (P/E) ratio of 11.71X. That is above the trade’s 10.02X, reflecting a stretched valuation.

Value-to-Earnings F12M

Picture Supply: Zacks Funding Analysis

Evaluating Capital One Inventory Forward of This fall Earnings

Capital One’s bank card enterprise stands out as a core earnings engine, underpinned by its scale, data-driven underwriting and powerful model presence within the U.S. shopper finance market.

The acquisition of Uncover Monetary in Could 2025 (which reshaped the panorama of the bank card trade, making a behemoth and unlocking substantial worth for shareholders) has positioned COF to seize a bigger share of card spending. Thus, given its stable bank card and on-line banking companies, the corporate’s income prospects look encouraging.

Furthermore, as one of many largest bank card issuers within the nation, COF advantages from a diversified buyer base that spans prime to subprime segments, permitting it to generate enticing yields whereas actively managing dangers.

Whereas near-term outcomes could also be influenced by provisioning tendencies and macro circumstances, the long-term outlook for COF is supported by its disciplined threat administration, sturdy shopper spending engagement, and potential margin enlargement from scale and integration advantages.

Nevertheless, given the corporate’s investments in know-how and infrastructure, in addition to its inorganic enlargement efforts, total bills are anticipated to stay elevated within the close to time period, hurting bottom-line progress. Thus, traders mustn’t rush to purchase the COF inventory now. But, those that already personal the inventory of their portfolios ought to maintain on to it for long-term positive aspects.

Quantum Computing Shares Set To Soar

Synthetic intelligence has already reshaped the funding panorama, and its convergence with quantum computing may result in essentially the most important wealth-building alternatives of our time.

As we speak, you could have an opportunity to place your portfolio on the forefront of this technological revolution. In our pressing particular report, Past AI: The Quantum Leap in Computing Energy, you may uncover the little-known shares we consider will win the quantum computing race and ship huge positive aspects to early traders.

Wells Fargo & Firm (WFC) : Free Inventory Evaluation Report

Citigroup Inc. (C) : Free Inventory Evaluation Report

Capital One Monetary Company (COF) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.