Palantir Applied sciences PLTR has emerged as one of many strongest-performing enterprise software program and synthetic intelligence shares over the previous 12 months, delivering a rise of greater than 120% and dramatically outperforming its broader trade.

Picture Supply: Zacks Funding Analysis

Whereas the inventory has seen a modest pullback in current months, this seems to be a wholesome consolidation somewhat than a deterioration in fundamentals. A better take a look at Palantir’s expertise, monetary execution, and progress trajectory means that the long-term funding case stays firmly intact.

In contrast to many AI-focused firms racing to construct ever-larger fashions, Palantir occupies a differentiated and defensible place. The corporate focuses on enabling organizations to deploy AI at scale inside actual operational environments, making it a important infrastructure supplier somewhat than a speculative expertise vendor.

PLTR’s Synthetic Intelligence Platform

On the coronary heart of Palantir’s technique is its Synthetic Intelligence Platform, which permits organizations to construction, combine, and govern advanced datasets so AI techniques can function successfully. Enterprises sometimes wrestle with fragmented knowledge throughout finance, operations, provide chains and human assets. PLTR solves this downside utilizing an ontology-based structure that creates a digital twin of a company’s operations.

This design permits AI to work together immediately with enterprise workflows somewhat than producing disconnected insights. In consequence, Palantir is positioned on the demand aspect of the AI economic system, the place monetization is dependent upon execution and outcomes somewhat than uncooked computing energy. This distinction is more and more vital as enterprises shift from AI experimentation to production-scale deployments.

Foundry Driving Explosive Industrial Development

Foundry has turn out to be Palantir’s major progress engine within the business market. The platform integrates knowledge from ERP techniques, IoT sensors and enterprise databases utilizing greater than 200 prebuilt connectors. Automated, low-code pipelines permit firms to unify structured and unstructured knowledge rapidly, whereas embedded analytics and machine studying instruments help use circumstances corresponding to provide chain optimization, fraud detection and predictive upkeep.

The business momentum behind Foundry is accelerating quickly. In the latest quarter, Palantir’s U.S. business revenues surged 121% 12 months over 12 months, highlighting rising enterprise demand for operational AI options. General, U.S. revenues rose 77% 12 months over 12 months, considerably outpacing worldwide progress and reinforcing the energy of the home market.

Buyer enlargement can be deepening. Palantir closed greater than 200 offers exceeding $1 million in worth throughout the quarter, together with dozens of contracts above $5 million and $10 million. This displays not solely new buyer wins but in addition broader adoption throughout present purchasers. The August launch of Foundry DevOps additional strengthens the platform by simplifying utility deployment and lifecycle administration, decreasing friction for enterprise customers.

Gotham Offers Stability and Strategic Credibility

Whereas Foundry fuels business enlargement, Gotham stays a cornerstone of Palantir’s enterprise. Gotham is designed for mission-critical intelligence purposes, integrating huge datasets in actual time and making use of AI-driven analytics to establish threats, detect anomalies and improve situational consciousness.

Gotham’s continued adoption by authorities and protection businesses supplies Palantir with long-term income stability and exceptionally excessive switching prices. These relationships additionally improve Palantir’s credibility with business clients, significantly in regulated industries corresponding to healthcare, finance and vitality. Few firms can efficiently serve each public-sector intelligence businesses and huge enterprises, giving Palantir a novel aggressive benefit.

Collectively, Foundry and Gotham type a dual-platform technique that balances high-growth business alternatives with sturdy public-sector contracts.

Sturdy Monetary Efficiency and Increasing Margins

Palantir’s current monetary efficiency underscores the scalability of its software program mannequin. Within the third quarter of 2025, whole revenues elevated 63% 12 months over 12 months, pushed primarily by U.S. business demand. The corporate achieved an adjusted working margin of 51%, its highest degree thus far, reflecting sturdy working leverage and disciplined value administration.

Profitability can be bettering on a GAAP foundation. Working earnings reached $393 million, whereas web earnings rose to $476 million. Earnings per share elevated greater than 100% 12 months over 12 months, demonstrating that Palantir’s progress is translating into bottom-line outcomes somewhat than being consumed by rising bills.

The steadiness sheet additional strengthens the funding case. Palantir ended the quarter with roughly $6.4 billion in money and equivalents and no debt, offering substantial flexibility to spend money on innovation, pursue strategic initiatives and face up to macroeconomic uncertainty.

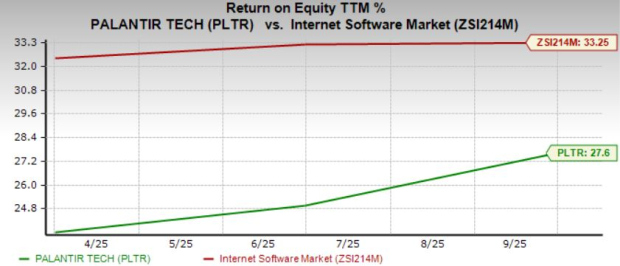

Return on Fairness Displays Lengthy-Time period Technique

Palantir at the moment generates a return on fairness of roughly 28%, barely under the trade common of 33% however nonetheless indicative of sturdy capital effectivity. Importantly, this metric displays administration’s deliberate choice to prioritize platform enlargement and long-term scale over short-term optimization.

Picture Supply: Zacks Funding Analysis

Picture Supply: Zacks Funding Analysis

As investments in product growth and buyer deployment mature, working leverage is predicted to extend additional, offering a pathway for return on fairness enlargement. For long-term buyers, immediately’s ROE represents a basis somewhat than a ceiling.

Earnings Outlook and Analyst Help

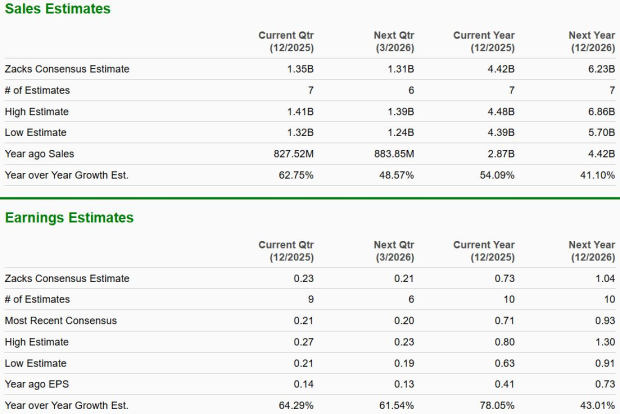

Earnings expectations for Palantir stay extremely favorable. The consensus estimate signifies sturdy year-over-year earnings progress for each the present quarter and the subsequent two fiscal years, supported by accelerating business adoption and increasing margins.

The Zacks Consensus Estimate for Palantir’s fourth-quarter 2025 earnings stands at 23 cents per share, suggesting 64.3% year-over-year progress. For 2025 and 2026, earnings are projected to rise 78% and 43%, respectively, in comparison with prior-year figures. Gross sales are additionally anticipated to see sturdy progress, growing 62.8% within the fourth quarter of 2025, with full-year gross sales projected to rise 54% in 2025 and 41% in 2026.

Picture Supply: Zacks Funding Analysis

PLTR, NVDA and AI: The Trio Main AI Revolution

Palantir is using the broader AI surge with friends like NVIDIA NVDA and C3.ai AI. NVIDIA is the undisputed spine of AI infrastructure, continues to see insatiable demand for its GPUs, whereas C3.ai is increasing its enterprise footprint. Whereas PLTR excels in deployment, NVIDIA powers the backend and C3.ai tackles the front-end utility layer. For buyers bullish on PLTR, NVDA’s dominance and C3.ai’s evolving technique stay price watching as this transformative tech cycle unfolds.

Conclusion

Palantir stands out as a uncommon mixture of fast progress, bettering profitability, and strategic relevance within the enterprise AI panorama. With Foundry driving explosive business enlargement, Gotham anchoring long-term stability, and a debt-free steadiness sheet supporting continued funding, the corporate is properly positioned for sustained worth creation. Whereas near-term volatility is feasible following a powerful rally, Palantir’s fundamentals proceed to strengthen. For buyers searching for publicity to scalable, mission-critical AI infrastructure, Palantir stays a purchase with a compelling long-term outlook.

PLTR inventory at the moment sports activities a Zacks Rank #1 (Sturdy Purchase). You may see the whole listing of immediately’s Zacks #1 Rank shares right here.

Zacks’ Analysis Chief Picks Inventory Most More likely to “At Least Double”

Our consultants have revealed their High 5 suggestions with money-doubling potential – and Director of Analysis Sheraz Mian believes one is superior to the others. In fact, all our picks aren’t winners however this one might far surpass earlier suggestions like Hims & Hers Well being, which shot up +209%.

See Our High Inventory to Double (Plus 4 Runners Up) >>

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

C3.ai, Inc. (AI) : Free Inventory Evaluation Report

Palantir Applied sciences Inc. (PLTR) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.