Latest declines in U.S. shares could also be regarding as a result of they defy the historic Santa Claus rally. Nevertheless, general, the key indexes posted stable good points in 2025, regardless of the April sell-off triggered by President Trump’s sweeping tariff declarations.

Now, they’re even higher positioned to construct momentum because of the “January Impact,” a seasonal tendency for shares to rise all through January. Inventory costs typically acquire momentum as buyers reinvest year-end bonuses and interact in tax-loss harvesting, which ends up in renewed shopping for within the markets.

Due to this fact, it’s prudent for astute buyers to capitalize on this bullish development by investing in growth-oriented shares. Many of those alternatives are concentrated within the know-how sector, which has gained considerably from the factitious intelligence (AI) increase, the primary power driving market progress for a while. Notable amongst them are NVIDIA Company NVDA, Micron Know-how, Inc. MU and Palantir Applied sciences Inc. PLTR. Let’s see why they’re positioned for progress and what makes them a compelling purchase –

NVIDIA Set for Sturdy Progress on AI Demand and Commerce Easing

NVIDIA’s sturdy aggressive edge within the AI {hardware} section and chronic demand for its next-generation Blackwell chips and cloud graphics processing models (GPUs) are set to drive progress.

Currently, the Trump administration has authorised shipments of H200 AI chips to pick out clients in China forward of the Lunar New 12 months vacation, indicating stable progress prospects. This transfer additionally means that U.S.-China commerce tensions have eased to some extent, a improvement welcomed by NVIDIA and different semiconductor corporations.

In the meantime, NVIDIA expects international knowledge heart capital outlays to extend 12 months after 12 months, supporting sturdy demand for its sought-after computing {hardware}. All of this has led NVIDIA to venture fiscal fourth-quarter 2026 revenues at round $65 billion, with a margin of plus or minus 2%, in accordance with investor.nvidia.com.

The corporate’s anticipated earnings progress fee for the present 12 months is 55.9%. The corporate’s $4.66 Zacks Consensus Estimate for earnings per share (EPS) is up 12% 12 months over 12 months, and NVIDIA has a Zacks Rank #1 (Sturdy Purchase). You may see the whole checklist of right this moment’s Zacks Rank #1 shares right here.

Picture Supply: Zacks Funding Analysis

Micron Set for Progress on HBM Demand and Sturdy Money Place

Micron’s high-bandwidth reminiscence (HBM) chips are in steady demand as a result of they deal with massive volumes of information whereas decreasing energy consumption. These chips weren’t solely a progress driver for Sanjay Mehrotra-led semiconductor behemoth in 2025 however will proceed to gas progress this 12 months.

The corporate expects fiscal second-quarter 2026 revenues between $18.3 billion and $19.1 billion, citing buyers.micron.com, almost mirroring the income progress seen in the course of the dot-com bubble. Moreover, Micron has a ample money steadiness of $3.9 billion from its fiscal first-quarter 2026, offering ample sources to assist its progress initiatives.

Thus, the corporate’s projected earnings progress fee for the present 12 months is 278.3%. The corporate’s $31.36 Zacks Consensus Estimate for EPS is up 185.9% year-over-year, and Micron has a Zacks Rank #1 (learn extra: Micron’s Blowout Earnings: The Finest AI Inventory for 2026?).

Picture Supply: Zacks Funding Analysis

Palantir Set for Progress as AIP Features Traction

Palantir is poised for progress because of the growing adoption of its Synthetic Intelligence Platform (AIP) amongst each U.S. authorities and industrial shoppers. AIP has turn out to be well-liked for its potential to seamlessly combine AI with advanced real-world knowledge and workflows, enabling quicker and extra knowledgeable decision-making.

Palantir expects income progress for each the U.S. authorities and industrial shopper segments and tasks whole revenues for 2025 between $4.396 billion and $4.400 billion, as cited on buyers.palantir.com.

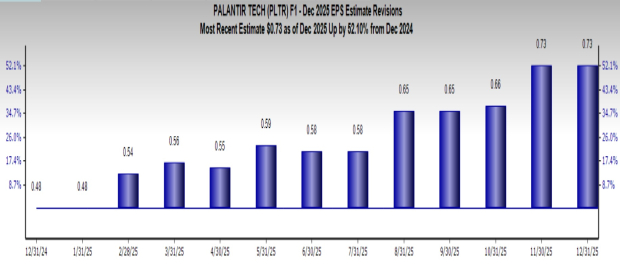

What’s extra, Palantir expects progress to proceed because of the increasing U.S. industrial and authorities clientele. In consequence, the corporate’s anticipated earnings progress fee for the present 12 months is 42.5%. The corporate’s $0.73 Zacks Consensus Estimate for EPS is up 52.1% 12 months over 12 months, and Palantir has a Zacks Rank #2.

Picture Supply: Zacks Funding Analysis

Analysis Chief Names “Single Finest Decide to Double”

From hundreds of shares, 5 Zacks specialists every have chosen their favourite to skyrocket +100% or extra in months to return. From these 5, Director of Analysis Sheraz Mian hand-picks one to have probably the most explosive upside of all.

This firm targets millennial and Gen Z audiences, producing almost $1 billion in income final quarter alone. A latest pullback makes now a super time to leap aboard. In fact, all our elite picks aren’t winners however this one might far surpass earlier Zacks’ Shares Set to Double like Nano-X Imaging which shot up +129.6% in little greater than 9 months.

Free: See Our High Inventory And 4 Runners Up

Micron Know-how, Inc. (MU) : Free Inventory Evaluation Report

NVIDIA Company (NVDA) : Free Inventory Evaluation Report

Palantir Applied sciences Inc. (PLTR) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.