The world’s largest semiconductor foundry, Taiwan Semiconductor (TSM), delivered one other distinctive quarterly earnings report this morning, reinforcing the energy and sturdiness of the worldwide AI funding cycle.

- In US {dollars}, second quarter income was $40.20 billion, which elevated 33.7% year-over-year and elevated 12.0% from the earlier quarter.

- Raised full-year 2026 income progress steerage to barely above 40% in US greenback phrases, up from its earlier projection of 30%.

- Chips utilizing superior applied sciences (7-nanometer and beneath) accounted for 77% of wafer income.

- Alongside thefinancial information TSMC introduced a further $100 billion funding plan for its Arizona fabrication crops, for a complete of $265 billion.

Altogether, this was a extremely encouraging replace on the enterprise, with broad implications for the endurance of the AI increase. Whereas buyers have grown more and more involved in regards to the scale of hyperscaler spending, and the rising use of debt to fund that funding, TSMC seems greater than snug increasing capability and shifting nearer to the supply of demand.

As a essential piece of infrastructure supporting the AI buildout, TSM shares have compounded at a rare annualized fee of 61.6% because the starting of 2023, producing a complete return of roughly 450%. Regardless of the sturdy report, the inventory is down ~3% as of this writing.

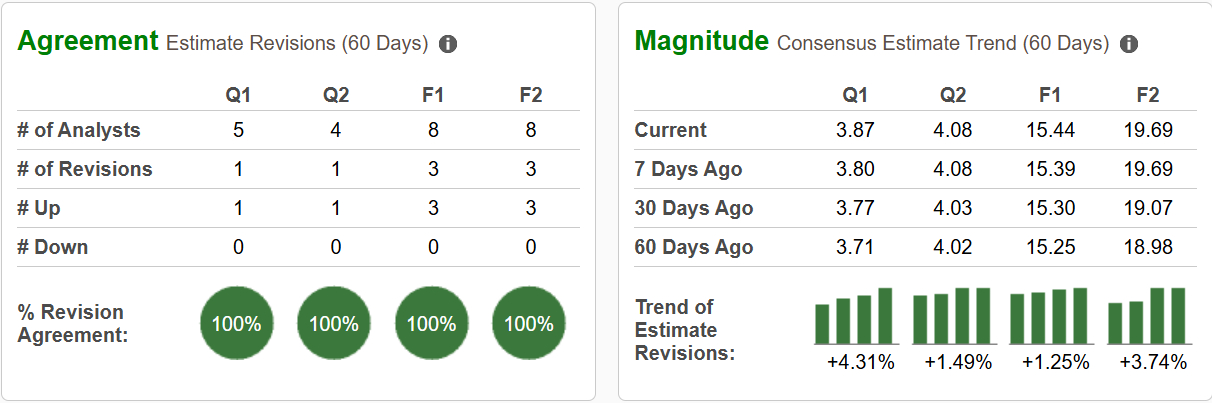

Picture Supply: Zacks Funding Analysis

Ought to Buyers Be Promoting TSM Shares too?

With TSM shares promoting off following the earnings report, buyers could also be questioning whether or not they need to observe the market’s lead. Nevertheless, given the corporate’s central position within the AI buildout and broader semiconductor trade, the weak point is extra probably a bout of profit-taking after a robust run, compounded by renewed skepticism and promoting throughout the AI commerce.

Taiwan Semiconductor’s outlook is undoubtedly tied to the continued growth of the AI increase. Even so, its present progress forecasts stay compelling, notably within the context of the inventory’s valuation. Gross sales are anticipated to develop 32% this 12 months and one other 27% subsequent 12 months, whereas earnings are projected to rise 45% this 12 months and 27.5% subsequent 12 months.

Regardless of that progress, TSM trades at roughly 27x ahead earnings, giving the inventory a PEG ratio close to 1. With highly effective thematic momentum behind the enterprise and manufacturing capability increasing in america, there can also be room for valuation a number of growth on high of the anticipated earnings progress.

Moreover, TSM carries a Zacks Rank #2 (Purchase), reflecting optimistic earnings estimate momentum. Over the previous 30 days, analysts have unanimously raised their estimates throughout the board, reinforcing the energy of the corporate’s near-term outlook.

Picture Supply: Zacks Funding Analysis

The AI Pendulum Swings Again Towards Skepticism

All through the AI increase, investor sentiment has repeatedly swung between exuberance and skepticism. Sturdy advances encourage more and more aggressive expectations, which finally give technique to issues about overspending, competitors and unsure returns on funding. These resets can produce sharp volatility even when the underlying progress cycle stays intact.

TSMC’s outcomes counsel that the present weak point remains to be extra of a sentiment and positioning correction than a deterioration within the elementary AI thesis. The inventory may have time to digest its good points, however accelerating income progress, rising estimates and one other main capability dedication point out that demand stays sturdy.

That outlook would change if hyperscalers started materially decreasing capital expenditures or if TSMC confirmed indicators of extra capability and weakening advanced-chip demand. For now, nevertheless, the pendulum seems to be swinging towards extreme pessimism whilst the corporate’s working efficiency continues to strengthen.

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our crew of consultants has simply launched the 5 shares with the best likelihood of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This high decide is a little-known satellite-based communications agency. House is projected to change into a trillion greenback trade, and this firm’s buyer base is rising quick. Analysts have forecasted a serious income breakout in 2025. In fact, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our Prime Inventory And 4 Runners Up

Taiwan Semiconductor Manufacturing Firm Ltd. (TSM) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.