The inventory market’s advance from late March by means of early July produced a number of main winners, however few had been extra spectacular than Micron Expertise (MU) and Marvell Expertise (MRVL). Each shares greater than tripled from their spring lows as buyers rushed into corporations positioned at essential factors throughout the AI infrastructure buildout.

Micron benefited from surging demand for high-bandwidth reminiscence, a essential part for AI inference, the quickest rising requirement for LLMs. Reminiscence has traditionally been one of the crucial commoditized and cyclical areas of the semiconductor trade. However as demand started overwhelming obtainable provide, Micron discovered itself controlling one of many scarcest sources within the AI ecosystem. Pricing energy adopted, earnings estimates soared and the inventory responded accordingly.

Marvell’s rally was equally dramatic. The corporate was already benefiting from speedy development throughout customized silicon, interconnects, switching and optical networking, which is the plumbing that enables more and more giant AI information facilities to perform. Then Nvidia CEO Jensen Huang added gasoline to the transfer by figuring out Marvell as a possible future trillion-dollar firm.

However after extraordinary three-month runs, each shares have reversed sharply. Micron is now greater than 20% beneath its latest excessive, whereas Marvell has fallen greater than 35%.

So, is it time to purchase the pullback?

Not fairly. Micron is approaching a doubtlessly enticing setup, however Marvell doubtless wants extra time to stabilize.

The AI Sentiment Pendulum Swings Once more

I don’t consider the AI increase is ending. Nevertheless, it appears the narrative pendulum had swung too far towards exuberance, and intervals of maximum optimism sometimes require a significant reset earlier than the subsequent sustainable advance can start.

We’ve seen this sample a number of occasions all through the AI increase. Considerations about capital spending, cheaper Chinese language fashions, declining inference prices, aggressive threats and unsure returns on funding have repeatedly triggered sharp pullbacks.

Every concern has some benefit. The biggest expertise corporations are spending unprecedented quantities on AI infrastructure, whereas the final word economics of many AI companies stay unsure. However related doubts have emerged earlier than, and the broader semiconductor cycle has persistently resumed its advance after expectations and positioning cooled.

The method is rarely as clear as a theoretical mannequin. Sentiment strikes between enthusiasm and skepticism, producing irregular peaks and drawdowns round a longer-term pattern. Thus far, nevertheless, every main cycle inside the AI commerce has finally resolved greater.

Picture Supply: Zacks Funding Analysis

Given the scale of the latest declines and the sharp reversal in sentiment, I think the semiconductor correction is now nearer to its finish than its starting. That doesn’t imply the ultimate low is already in. The group might nonetheless expertise one other leg decrease, however a lot of the surplus enthusiasm is leaving, and the risk-reward profile is turning into extra constructive as expectations reset.

That doesn’t imply each pullback ought to be bought instantly. The underlying pattern can stay intact whereas particular person shares decline additional, consolidate for months or completely lose management. Buyers nonetheless want to differentiate between a sturdy enterprise inflection and a inventory that merely ran too far forward of itself.

MU and MRVL Have been Elementary Rallies, Not Pure Hypothesis

You will need to acknowledge that the advances in Micron and Marvell had been supported by real enterprise development.

I highlighted each corporations properly earlier than their most up-to-date rallies. Final summer time, I mentioned Marvell’s compelling long-term setup following a disappointing earnings response on this interview. I additionally recognized Micron as a non-consensus AI winner right here close to the start of what turned a rare advance.

The basics subsequently exceeded even optimistic expectations.

That separates the present scenario from a purely speculative bubble. Buyers weren’t merely bidding up unprofitable corporations based mostly on distant guarantees. Micron and Marvell produced substantial income development, quickly bettering earnings and publicity to areas of the AI provide chain the place demand stays sturdy.

Nonetheless, even essentially justified rallies can overshoot. After strikes of this magnitude, extra air may have to come back out earlier than both inventory is prepared for its subsequent sustained leg greater.

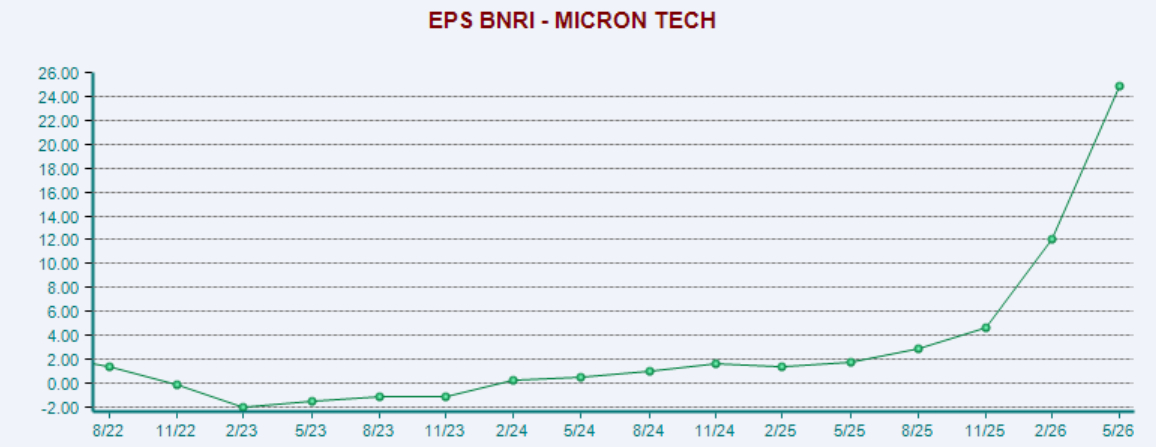

Micron’s Unbelievable Earnings Development

Micron’s latest monetary efficiency has been distinctive and helps clarify why the inventory gained a lot so shortly.

In fiscal Q3 2026, ended Could 28, Micron earned $25.11 per share on a non-GAAP foundation, up greater than 1,200% from $1.91 one 12 months earlier. Income elevated 346%, climbing from $9.30 billion to $41.46 billion.

Picture Supply: Zacks Funding Analysis

The corporate’s outlook recommended that the acceleration was not completed. Administration guided fiscal This fall income to roughly $50 billion, with non-GAAP earnings approaching $31 per share. Each would signify data by huge margins.

Micron’s earnings revisions have been equally exceptional. In keeping with Goldman Sachs, the corporate accounted for roughly 51% of all S&P 500 earnings-per-share revisions throughout the latest interval it measured. That’s an astounding contribution from one firm and demonstrates how aggressively expectations have been repriced round reminiscence demand.

However that focus additionally creates danger.

Micron is not an neglected AI beneficiary. Buyers now broadly perceive the high-bandwidth-memory scarcity, the corporate’s pricing energy and the size of its earnings development. Future features will more and more depend upon whether or not Micron can proceed exceeding already elevated expectations.

The corporate additionally stays uncovered to the reminiscence cycle. AI might have created one thing nearer to a silicon super-cycle, however provide ultimately responds to excessive costs. Prospects can alter spending, opponents can develop manufacturing and exceptionally sturdy margins can entice further capability.

Technically, Micron is now testing an necessary help space. The inventory has not but damaged its broader uptrend, however a decisive transfer beneath that stage would weaken the setup and recommend that the reset has additional to run.

For buyers concerned with shopping for the pullback, Micron is the extra compelling of the 2 shares. Nevertheless, I’d nonetheless watch for proof that help is holding and volatility is starting to say no fairly than attempting to foretell the precise backside.

Picture Supply: TradingView

Jensen Huang’s Trillion-Greenback Name on Marvell

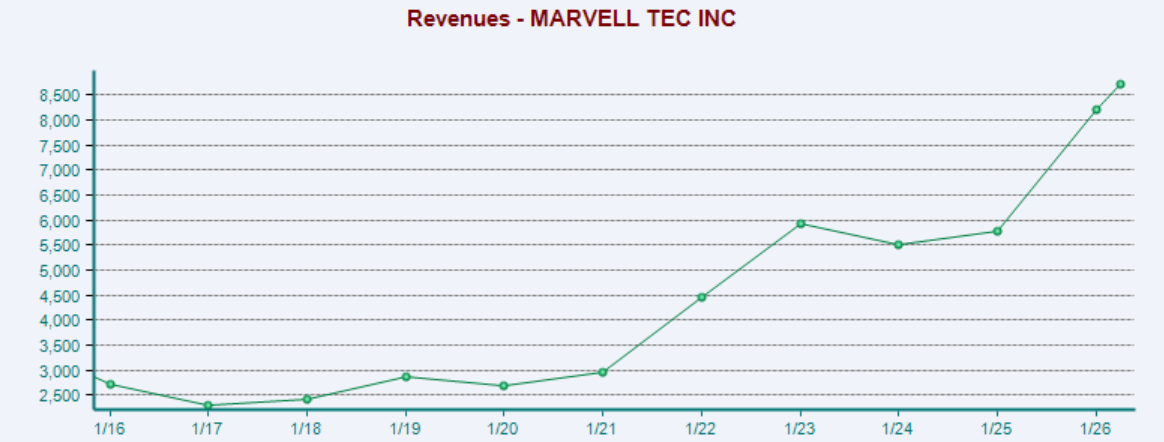

Marvell has additionally delivered unusually sturdy development, though its underlying inflection started properly earlier than the inventory’s most up-to-date surge.

For a time, that enchancment was hidden beneath weak headline outcomes. Complete income barely elevated from $5.5 billion in fiscal 2024 to $5.77 billion in fiscal 2025 as deep downturns in Marvell’s legacy service and enterprise companies offset speedy data-center development.

One layer beneath the headline numbers, nevertheless, the transformation was already underway.

Knowledge-center income grew 88% in fiscal 2025 and represented roughly 75% of the corporate’s enterprise by year-end, up from roughly 50%. Customized AI silicon entered quantity manufacturing whereas Marvell’s electro-optics enterprise continued supplying the connectivity required to maneuver information throughout more and more complicated AI methods.

As soon as the weak point within the legacy companies started to ease, the underlying development turned seen within the consolidated outcomes.

Fiscal 2026 income reached a document $8.2 billion, representing development of 42%, whereas data-center income surpassed $6 billion. Non-GAAP earnings rose 81% to $2.84 per share, and financial Q1 2027 income elevated one other 28%.

Picture Supply: Zacks Funding Analysis

These outcomes assist clarify why Marvell has turn into a distinguished AI infrastructure corporations. The enterprise spans a number of necessary areas, together with customized accelerators, optical connectivity, switching and data-center interconnects.

However the valuation leaves little room for disappointment.

Marvell trades at greater than 50x ahead earnings, though long-term earnings development forecasts are additionally close to 50%. That mixture can help a premium a number of, however solely whereas development stays distinctive and execution persistently exceeds expectations.

Marvell might ultimately turn into a trillion-dollar firm, however getting there would require years of extraordinary compounding. Even at an elevated a number of, a $1 trillion valuation would suggest roughly $20 billion in annual revenue. That is a gigantic leap from the corporate’s present earnings base.

For that motive, I’d not deal with the trillion-dollar prediction as a near-term funding thesis. It’s higher understood as an expression of Marvell’s strategic significance inside the AI infrastructure ecosystem.

The fast technical image is much less encouraging. Momentum has shifted decisively decrease, volatility stays elevated and the inventory has not but established a transparent help stage. Quite than shopping for just because Marvell is 35% beneath its excessive, I’d watch for seen base-building, tighter buying and selling ranges and proof that sellers have gotten exhausted.

Picture Supply: TradingView

Micron Is Nearer to a Purchase Than Marvell

Each shares stay tied to highly effective long-term tendencies, however the dangers are totally different.

Micron’s major danger is the sturdiness of the reminiscence cycle. Buyers should decide how lengthy high-bandwidth-memory demand can outpace provide and whether or not distinctive pricing and margins can persist as manufacturing expands.

Marvell’s major dangers are valuation and execution. The corporate should proceed changing its sturdy positioning in customized silicon and connectivity into earnings development enough to justify a premium a number of.

Micron at the moment presents the extra enticing setup as a result of its earnings momentum is stronger and the inventory is testing a clearly outlined technical stage. Marvell has skilled a extra critical momentum breakdown and certain wants an extended interval of stabilization.

That doesn’t imply Micron ought to be bought indiscriminately. A break beneath help might create one other significant leg decrease, notably if broader semiconductor sentiment continues deteriorating.

For now, I’d classify Micron as a inventory to observe intently close to help. Marvell stays a inventory to attend on till its volatility declines and a reputable base begins to type.

How Buyers Can Strategy MU and MRVL

The latest declines in Micron and Marvell look extra like sentiment resets than proof that the AI infrastructure increase is breaking. Their rallies had been supported by reputable enterprise development, extraordinary earnings momentum and publicity to among the most strategically necessary elements of the semiconductor trade.

However sturdy companies don’t robotically turn into enticing shares at each worth.

The narrative pendulum is now swinging away from exuberance and again towards skepticism. That course of might proceed for a number of weeks or months as buyers query AI spending, future returns and whether or not the trade has expanded capability too aggressively.

Micron is nearer to an actionable entry, however buyers ought to first search for help to carry and buying and selling circumstances to stabilize. Marvell carries a extra demanding valuation and has suffered a extra decisive technical breakdown, making persistence particularly necessary.

The bigger AI alternative doubtless stays intact. However after rallies of this magnitude, buyers don’t have to rush. MU is a watch close to help, whereas MRVL stays a wait. A sturdy backside might ultimately create enticing alternatives in each, however neither inventory has totally accomplished its reset.

Radical New Expertise May Hand Buyers Big Beneficial properties

Quantum Computing is the subsequent technological revolution, and it could possibly be much more superior than AI.

Whereas some believed the expertise was years away, it’s already current and transferring quick. Giant hyperscalers, similar to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Prepare dinner reveals 7 rigorously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early specialists who acknowledged NVIDIA’s huge potential again in 2016. Now, he has keyed in on what could possibly be “the subsequent massive factor” in quantum computing supremacy. In the present day, you will have a uncommon probability to place your portfolio on the forefront of this chance.

See High Quantum Shares Now >>

Micron Expertise, Inc. (MU) : Free Inventory Evaluation Report

Marvell Expertise, Inc. (MRVL) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.