")

In a single type or one other, most traders already personal Alphabet (GOOG). As one of many world’s largest publicly traded firms, it ranks as a dominant holding in almost each main index and ETF. But regardless of its measurement and widespread possession, Alphabet stays a compelling addition to any traders portfolio.

Supported by contemporary earnings estimate revisions, robust value momentum, and a number one place throughout digital promoting, cloud computing, and synthetic intelligence, Alphabet continues to supply a pretty mixture of high quality, development, and affordable valuation. That is why it stays a core long-term holding and earns at the moment’s Bull of the Day.

Picture Supply: Zacks Funding Analysis

Alphabet Earnings Momentum Accelerates

Alphabet’s most up-to-date earnings report was a reminder that that is nonetheless one of many highest-quality companies on the planet. The corporate generated $109.9 billion in first-quarter income, up 22% from the prior 12 months, whereas working earnings rose 30% and working margin expanded to 36.1%. Google Cloud was a significant standout, with income surging 63% to $20.0 billion, as AI-driven enterprise demand continues to speed up.

That stage of development and margin growth is spectacular for any firm, however it’s particularly notable for a enterprise already working at Alphabet’s scale. Buyers might assume that mega-cap know-how firms finally lose the flexibility to compound at enticing charges, however Alphabet continues to show in any other case.

Earnings had been even stronger, with diluted EPS rising 82% 12 months over 12 months to $5.11. Whereas a part of that soar was helped by funding features, the core working efficiency was nonetheless glorious.

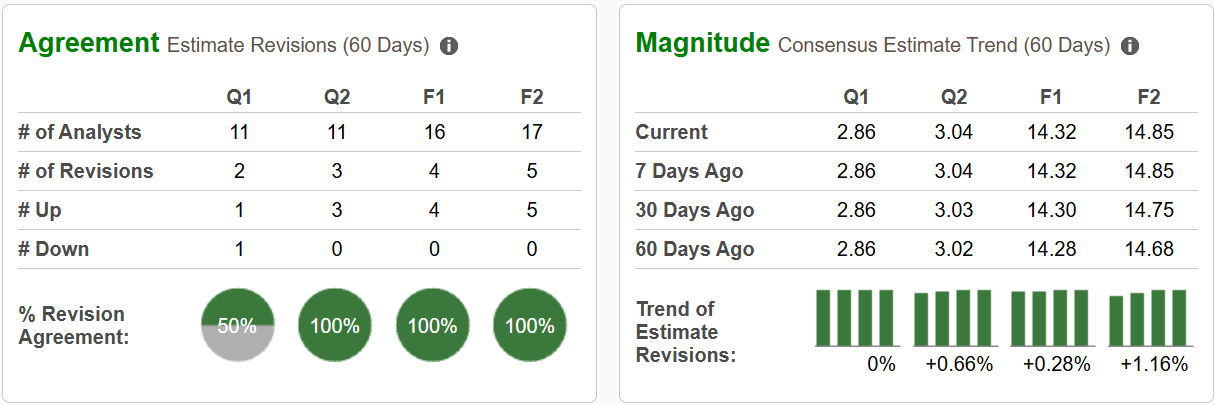

For an organization that has lengthy been seen as probably the most dependable earnings compounders available in the market, the newest report reinforces the case that Alphabet nonetheless has room to ship upside. This place has been reiterated by modest however current earnings upgrades, incomes it a Zacks Rank #1 (Robust Purchase) ranking.

Picture Supply: Zacks Funding Analysis

Search Stays the Core Revenue Engine

The largest concern round Alphabet during the last two years has been whether or not AI would disrupt Google Search. That concern is comprehensible. Search is without doubt one of the biggest enterprise fashions ever created, and any credible menace to that revenue engine deserves consideration.

However to date, Alphabet seems to be adapting slightly than fading. Search development has not merely held up underneath the rise of AI however accelerated. Google Search & different income grew roughly 10% 12 months over 12 months in Q1 2025, then improved to 12%, 15%, 17% and at last 19% in Q1 2026.

The reason being that Google nonetheless has deeply entrenched distribution, person behavior, advertiser relationships, information, infrastructure and product depth that few firms can match. Even when the search interface modifications over time, Alphabet stays one of many best-positioned firms to monetize that shift.

The AI transition might stress elements of the legacy search mannequin, however it additionally offers Google an opportunity to deepen engagement, enhance advertisements and develop the variety of use instances tied to its ecosystem. In different phrases, AI seems to not be a threat for Alphabet, however a core driver of development.

GOOG Inventory Nonetheless Seems to be Fairly Valued

Alphabet shouldn’t be as low cost because it was final 12 months, however the inventory nonetheless seems fairly valued relative to its mega-cap friends. GOOG trades at roughly 24.8x ahead earnings, beneath Apple at 36.1x and Amazon at 31.7x, whereas sitting in the identical basic vary as Nvidia and Meta.

That valuation seems honest, particularly as Alphabet’s fundamentals proceed to enhance. Search development has accelerated, Google Cloud is turning into a bigger revenue contributor, and the corporate continues to generate substantial free money circulate. With a mid-teens 3-5 12 months EPS development forecast, GOOG additionally screens fairly effectively on a PEG foundation.

Alphabet shouldn’t be the most affordable Magnificent Seven inventory, as Meta and Microsoft look considerably higher on valuation-to-growth, whereas Nvidia stays in a class of its personal if its development forecasts maintain. However in contrast with Apple and Amazon, Alphabet affords a really enticing steadiness of valuation, sturdiness and anticipated earnings development.

The inventory has re-rated increased from its early-2025 lows, reflecting its AI and {hardware} integration, however it nonetheless doesn’t look stretched. Buyers are paying a market-leader a number of, not a perfection a number of, for one of many strongest enterprise fashions in know-how.

Picture Supply: Zacks Funding Analysis

Ought to Buyers Purchase Shares in GOOG Inventory?

Alphabet shouldn’t be an undiscovered inventory, and that’s not the purpose. The purpose is that even after years of huge features, Alphabet stays probably the greatest companies on the planet and nonetheless affords a compelling setup for traders.

The corporate has dominant core property, accelerating Search development, rising Google Cloud profitability, main AI optionality, robust earnings momentum and a valuation that continues to be affordable relative to its peer group. The largest concern at the moment is whether or not Alphabet and the remainder of mega-cap tech are overextending themselves within the AI funding cycle. The corporate is spending aggressively on information facilities, chips and infrastructure, and traders will finally have to see these investments translate into sturdy income development, stronger margins and better earnings energy.

For now, Alphabet’s core enterprise stays robust, and the corporate seems to be evolving with the AI cycle slightly than being displaced by it. For traders searching for a high-quality know-how chief with a number of long-term development drivers, GOOG stays probably the most enticing names available in the market.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t more likely to maintain delivering the most important earnings. AI’s second wave is shifting from infrastructure to implementation and these firms are on the forefront of this transition, positioned to grow to be what Amazon and Google had been to the web period.

Alphabet Inc. (GOOG) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.