Johnson & Johnson JNJ) has quietly reemerged as one of many stronger-performing large-cap healthcare shares in 2026.

After hitting recent all-time highs of $269 a share final week, buyers are turning their consideration to the healthcare big’s Q2 report, which is scheduled for Wednesday, July 15, earlier than the opening bell.

Whereas many tech shares proceed to command premium valuations, Johnson & Johnson affords buyers a mixture of defensive traits, constant earnings progress, a premier dividend, and one of many strongest stability sheets in company America.

That mixture has helped gasoline current momentum, however the query now could be whether or not one other sturdy quarterly report can ship JNJ shares even increased after spiking greater than 20% 12 months up to now.

Picture Supply: Zacks Funding Analysis

Johnson & Johnson’s Q2 Expectations

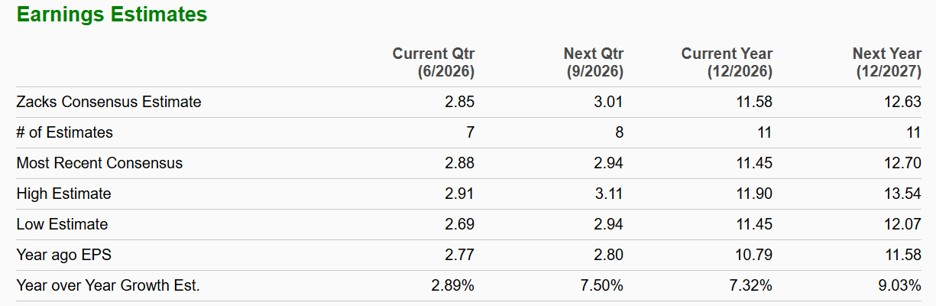

Wall Avenue expects Johnson & Johnson to submit one other strong quarter regardless of ongoing patent headwinds throughout parts of its pharmaceutical portfolio.

Consensus estimates presently name for Q2 EPS of roughly $2.85 on income of $25.18 billion, representing modest progress of three% and 6% from the prior-year quarter, respectively.

Buyers will possible be paying shut consideration to a number of key areas:

- Continued progress from the Progressive Medication section

- Gross sales of blockbuster most cancers therapies comparable to Darzalex, which continues to be considered one of J&J’s largest progress drivers

- Momentum within the MedTech enterprise, significantly cardiovascular merchandise

- Any updates to full-year steerage following the corporate’s stronger-than-expected first quarter

One other encouraging signal is that J&J continues to speculate aggressively in future progress. Latest pipeline developments, oncology growth, and strategic acquisitions have strengthened its long-term progress outlook whereas serving to offset future patent expirations.

The corporate additionally has one of many longest monitor data of exceeding earnings expectations, with a mean EPS shock of 1.89% in its final 4 quarterly studies.

Picture Supply: Zacks Funding Analysis

JNJ’s Valuation Nonetheless Seems Cheap

Regardless of not too long ago reaching new highs, Johnson & Johnson’s valuation stays comparatively enticing in comparison with many large-cap healthcare friends and the broader market.

JNJ presently trades at 22X ahead earnings, which is barely beneath the benchmark S&P 500 whereas buying and selling close to its Zacks Giant Cap Prescribed drugs Trade common of 20X.

Picture Supply: Zacks Funding Analysis

That valuation seems enticing contemplating the corporate’s:

- Diversified pharmaceutical portfolio

- Rising medical system enterprise

- Constant free money circulation era

- Distinctive stability sheet

- Secure earnings profile

Analysts additionally challenge adjusted EPS to proceed rising within the excessive single digits over the subsequent two fiscal years, supporting the argument that in the present day’s valuation is supported by bettering fundamentals fairly than speculative enthusiasm.

For long-term buyers in search of high quality fairly than speedy a number of growth, JNJ nonetheless affords a beautiful risk-reward profile.

Picture Supply: Zacks Funding Analysis

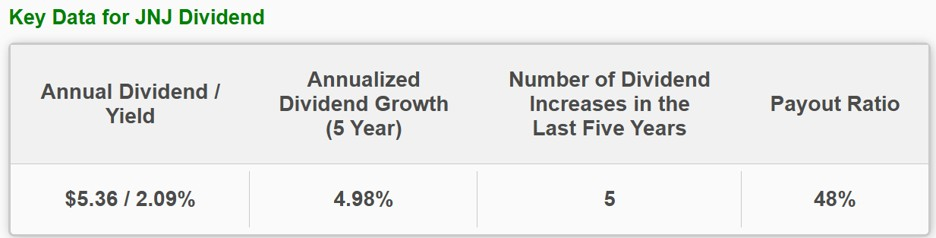

JNJ Stays a Dividend Powerhouse

Certainly one of JNJ’s largest funding sights stays its dividend.

Johnson & Johnson is a Dividend King, having elevated its dividend for greater than six consecutive a long time, making it one of many longest-running dividend progress tales available in the market.

JNJ’s dividend yield of two.09% is roughly on par with its {industry} common and stays comfortably above the S&P 500’s 1.03% common, whereas being supported by:

- Robust recurring money flows

- Funding-grade stability sheet

- Diversified healthcare operations

- Conservative payout ratio (48%)

Not like many high-yield firms that sacrifice progress to assist payouts, Johnson & Johnson has persistently demonstrated its potential to speculate closely in analysis, acquisitions, and innovation whereas persevering with to reward shareholders via annual dividend will increase.

For income-oriented buyers, that mixture of reliable dividend progress and capital appreciation potential stays tough to match amongst large-cap healthcare firms.

Picture Supply: Zacks Funding Analysis

Can JNJ Inventory Attain Greater Highs?

Momentum has clearly improved over the previous a number of weeks, with buyers rotating again towards high-quality defensive names because the Q2 earnings season approached.

If Johnson & Johnson delivers one other earnings beat, raises steerage, or supplies encouraging commentary surrounding its pharmaceutical pipeline and MedTech companies, the inventory may have room to increase its current breakout.

In fact, expectations have additionally risen following the current rally, that means administration’s steerage may show simply as necessary because the quarterly outcomes themselves.

Thankfully, Johnson & Johnson’s diversified enterprise mannequin has traditionally allowed it to navigate financial uncertainty higher than many firms, making it an interesting choice for buyers in search of regular long-term compounders fairly than extremely risky progress shares.

Backside Line

Johnson & Johnson might not ship the explosive upside of many AI leaders, however its mixture of earnings consistency, cheap valuation, industry-leading dividend progress, and bettering enterprise momentum continues to make the healthcare big a beautiful long-term holding.

A powerful Q2 report may present one other catalyst for JNJ shares to push towards recent highs, though a lot will depend upon administration’s outlook for the rest of 2026.

For now, Johnson & Johnson inventory presently lands a Zacks Rank #3 (Maintain), suggesting buyers might wish to await extra earnings estimate revisions following its upcoming Q2 report earlier than initiating or increasing positions.

Zacks’ Analysis Chief Names “Inventory Most Prone to Double”

Our workforce of consultants has simply launched the 5 shares with the best likelihood of gaining +100% or extra within the coming months. Of these 5, Director of Analysis Sheraz Mian highlights the one inventory set to climb highest.

This high choose is a little-known satellite-based communications agency. Area is projected to turn out to be a trillion greenback {industry}, and this firm’s buyer base is rising quick. Analysts have forecasted a significant income breakout in 2025. In fact, all our elite picks aren’t winners however this one may far surpass earlier Zacks’ Shares Set to Double like Hims & Hers Well being, which shot up +209%.

Free: See Our Prime Inventory And 4 Runners Up

Johnson & Johnson (JNJ) : Free Inventory Evaluation Report

This text initially revealed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.