Inventory Close to Highs Forward of Q2 Earnings: Purchase, Maintain, or Promote?")

Delta Air Traces DAL) has been one of many airline {industry}’s standout performers in 2026, with its inventory climbing greater than 20% YTD as traders have grown extra optimistic about premium journey demand, enhancing {industry} pricing, and easing gas price considerations.

With Delta scheduled to report Q2 outcomes earlier than the market opens on Friday, July 10, traders will likely be seeking to see whether or not the service can justify its robust rally and supply an encouraging outlook for the rest of the busy summer season journey season.

Picture Supply: Zacks Funding Analysis

Delta’s Q2 Expectations

Wall Road expects one other quarter of wholesome income development, pushed by resilient demand for worldwide routes, premium cabin bookings, and Delta’s increasing loyalty ecosystem.

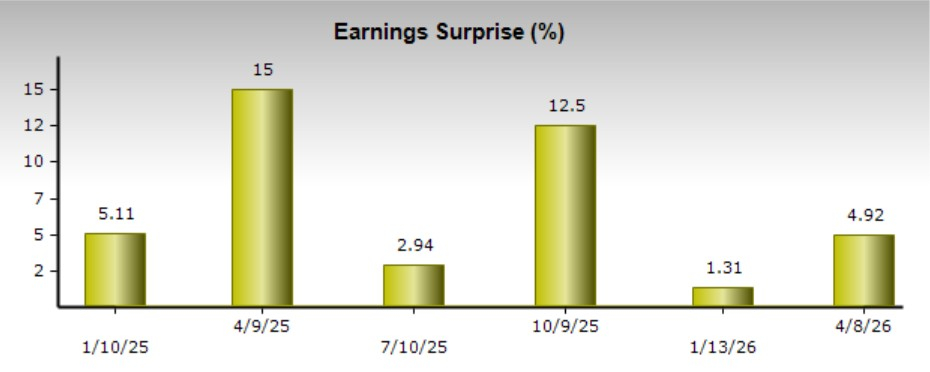

Present consensus estimates name for Q2 income of $17.74 billion, representing greater than 6% 12 months over 12 months development. Quarterly EPS is predicted at $1.50, down from final 12 months’s Q2 revenue of $2.10 per share as greater labor bills and elevated gas prices weigh on margins.

Though earnings are anticipated to say no from final 12 months’s exceptionally robust comparability, Delta has developed a powerful observe file of execution, exceeding EPS expectations for six consecutive quarters.

Picture Supply: Zacks Funding Analysis

Premium Demand Stays Delta’s Largest Energy

In contrast to many airways that stay closely depending on price-sensitive home leisure vacationers, Delta has more and more differentiated itself by premium choices and company journey.

Administration has emphasised:

- Premium seating demand

- Worldwide journey power

- Company journey restoration

- American Categorical AXP) loyalty partnership development

These higher-margin income streams have helped Delta generate extra steady profitability than a lot of its airline friends, at the same time as {industry} circumstances fluctuate. Analysts additionally anticipate premium journey demand to stay wholesome all through the summer season journey season.

Gas Prices and Steerage Will Be the Largest Story

Whereas traders will naturally deal with quarterly earnings, administration’s outlook could finally matter greater than the reported numbers.

Earlier this 12 months, Delta warned that gas bills would stay elevated throughout the June quarter, though declining oil costs in current weeks have improved the {industry}’s outlook heading into the second half of 2026.

Buyers will wish to monitor Delta’s commentary on:

- Third-quarter demand traits

- Company reserving exercise

- Worldwide journey demand

- Gas expense expectations

- Capability development

- Full-year earnings outlook

If administration strikes a assured tone, traders could turn into more and more optimistic about airline profitability heading into the rest of 2026.

Is Delta Inventory Nonetheless Fairly Valued?

Regardless of Delta’s spectacular YTD rally, DAL stays comparatively engaging in comparison with many large-cap firms.

Airline shares usually commerce at modest earnings multiples as a result of cyclical nature of the enterprise. Nevertheless, Delta has earned a premium valuation due to its industry-leading operational efficiency, robust steadiness sheet enhancements, premium buyer combine, and rising loyalty income.

At round $86 a share, DAL presently trades at 16X ahead earnings, with the Zacks Transportation-Airline Trade common at 11X. Notably, home rivals United Airways UAL) and American Airways AAL) are buying and selling at ahead earnings multiples of 12X and 37X, respectively.

Given its reasonable P/E valuation, the market could proceed to reward Delta if administration demonstrates that earnings development can stay sturdy regardless of macroeconomic uncertainty.

Picture Supply: Zacks Funding Analysis

Backside Line

Delta enters its Q2 report with appreciable momentum as journey demand has remained resilient and {industry} fundamentals proceed to enhance. Buyers will likely be searching for affirmation that premium journey, worldwide demand, and loyalty revenues are offsetting price pressures in hopes that administration gives constructive steerage for the rest of 2026.

That mentioned, a lot of the current optimism could already be mirrored within the share value following the inventory’s robust advance this 12 months. Whereas Delta stays one of many highest-quality names within the airline {industry}, traders could wish to await administration’s newest outlook earlier than turning into extra aggressive with DAL touchdown a Zacks Rank #3 (Maintain) in the intervening time.

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t prone to preserve delivering the most important earnings. AI’s second wave is shifting from infrastructure to implementation and these firms are on the forefront of this transition, positioned to turn into what Amazon and Google have been to the web period.

Delta Air Traces, Inc. (DAL) : Free Inventory Evaluation Report

United Airways Holdings Inc (UAL) : Free Inventory Evaluation Report

American Categorical Firm (AXP) : Free Inventory Evaluation Report

American Airways Group Inc. (AAL) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.