AI and chip shares tanked on Friday, sending the Nasdaq tumbling 4%. The bulls might dig their heels in once more early subsequent week. However there’s little doubt {that a} bigger pullback will occur sooner or later to supply a wholesome recalibration as a result of shares can solely climb so excessive earlier than the legal guidelines of market gravity take over.

This implies traders ought to begin shopping for tech shares proper now that haven’t rallied to new all-time highs alongside semiconductor and synthetic intelligence shares.

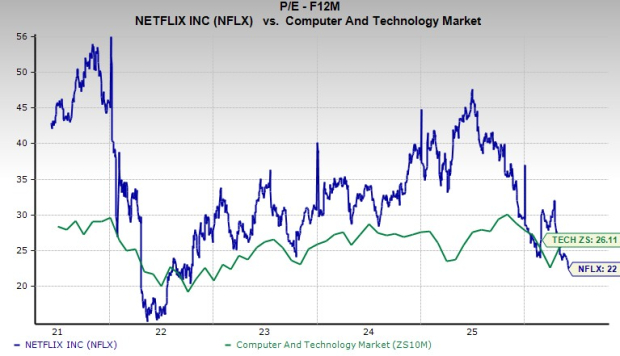

Netflix inventory is down virtually 40% from its 2025 highs to commerce at a reduction to the know-how sector (22X ahead earnings vs. 26.1X) regardless of crushing it during the last 10 and 20 years. The streaming leisure large is extra resilient to AI threats than many know-how companies, and Netflix is ready to develop its earnings by 42% in 2026 on 14% larger gross sales.

In the meantime, Uber has fallen 30% since October, and its common Zacks worth goal gives 48% upside from its present ranges. The ride-hailing firm’s long-term upside stays in place even because it faces attainable disruptions from tech companies seeking to seize their share of a attainable future filled with robotaxis and autonomous supply automobiles.

Picture Supply: Zacks Funding Analysis

Uber and Netflix are additionally seeking to discover help at some key technical ranges which may make them extra attractive for long-term traders since they provide sturdy progress that’s not based mostly on AI guarantees alongside stable worth in an overheated market.

Portfolio Rotation: Purchase Shares Outdoors AI and Semiconductors

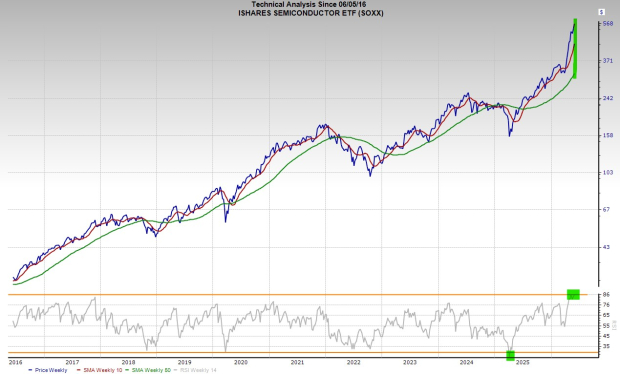

AI and chip shares look overheated within the brief run. For instance, the iShares Semiconductor ETF SOXX soared 95% between March 30 and June 4, taking it miles above its 10-week shifting common and to its most overbought RSI ranges in over a decade.

Some traders won’t need to chase AI and chip shares which have soared 50%, 100%, or 200% YTD (together with the massive fall on Friday).

Picture Supply: Zacks Funding Analysis

The subsequent pullback to a key technical degree may be scooped up relatively rapidly contemplating that the long-term AI outlook is bullish. It’s simply arduous to attempt to chase shares right here, particularly if Friday’s promoting triggers the beginning of a near-term selloff.

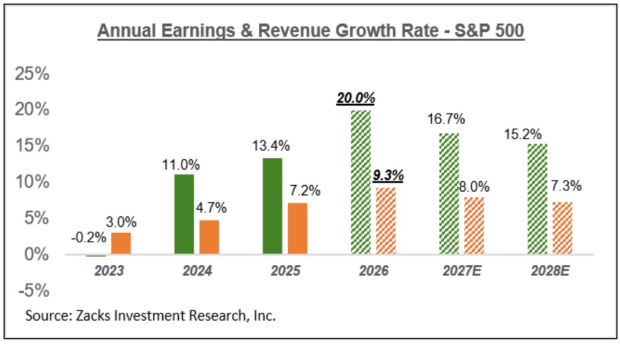

Fortunately, the long-term bull case for the inventory market stays firmly intact. Whole annual S&P 500 earnings are projected to develop 20% in 2026 on 9.3% larger gross sales, blowing away 2024 and 2025’s progress charges. The benchmark is projected to observe this up with 16.7% EPS enlargement subsequent 12 months and 15.2% larger in 2028.

Picture Supply: Zacks Funding Analysis

Extra importantly, all 16 Zacks sectors are projected to report YoY earnings progress in 2026, highlighting spectacular enlargement and financial resilience regardless of fears.

Purchase Tech Inventory Uber Now for Worth, Progress & 40% Upside

Uber Applied sciences, Inc.’s UBER core ride-hailing and supply companies are extra in style than ever, significantly amongst higher-income shoppers who’re much less impacted by inflation and financial cycles. The corporate can also be working a bodily enterprise that’s not going to be disrupted by AI. Uber is poised to thrive within the potential driverless car period via quite a few partnerships and past.

Uber’s gross bookings are projected to leap 21% in 2026, based mostly on our Zacks Key Firm Metrics information. Its month-to-month lively platform clients (MAPCs) are projected to climb 9% to 219.9 million in 2026, up from 202 million final 12 months, 171 million in 2024 (vs. 118 million in 2021).

Picture Supply: Zacks Funding Analysis

The agency has exploded in reputation because it supply enterprise and ride-hailing models achieve steam within the U.S. and globally. It grew its income 300% from the pre-Covid 2019 interval’s $13 billion to $52 billion in 2025. Trying forward, Uber is projected to develop its income by 11% in 2026 and over 15% subsequent 12 months to $66.6 billion.

The agency’s Uber One paid membership surpassed 50 million members globally within the first quarter of 2026, with “50% of Mobility and Supply Gross Bookings now generated by members.” Uber is increasing its enterprise through offers with Expedia to seize extra “on a regular basis shopper intent” throughout mobility, native commerce, and journey.

Picture Supply: Zacks Funding Analysis

It has additionally was a worthwhile firm by taking a bigger proportion of every journey/supply fare whereas optimizing pricing and driver funds, alongside different profitability efforts. Uber posted GAAP earnings per share of $4.73 a share in FY25 vs. a lack of -$4.69 a share in 2022.

That stated, its EPS progress is projected to take a success in 2026 because of a ramp-up in investments throughout autonomous automobiles/robotaxis, worldwide supply enlargement, AI efforts, and a key accounting change because of a enterprise mannequin change within the UK. Fortunately, it’s projected to bounce again and return to YoY progress in FY27 and past.

Picture Supply: Zacks Funding Analysis

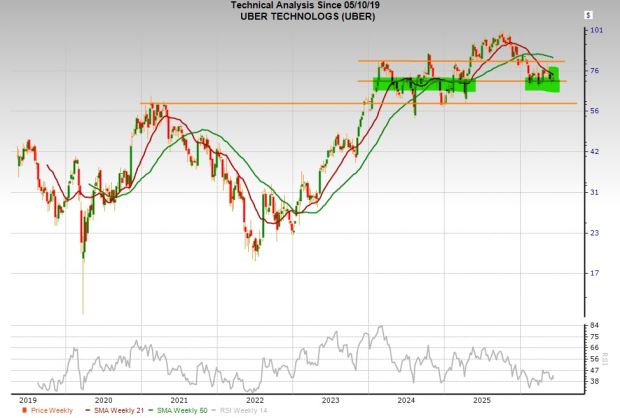

Uber inventory has dropped 30% from its October 2025 highs. The inventory has climbed 70% since going public in Might 2019. It’s attempting to carry its floor on the key technical vary above, whereas attempting to lastly climb again above its 21-week shifting common.

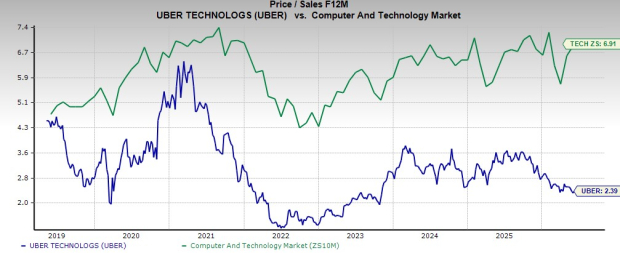

Uber is buying and selling 95% beneath its highs and 22% beneath Tech at 20.2X ahead earnings. It additionally trades at a 65% low cost to Tech and 60% in opposition to its peaks at 2.4X ahead gross sales. Uber’s common Zacks worth goal gives 48% upside from its present $70.71 a share.

NFLX: Purchase This Tech Inventory Now and Maintain Without end?

Netflix, Inc. NFLX inventory has fallen ~40% from its summer time 2025 highs, offering traders with an awesome likelihood to purchase a confirmed tech large that is progress isn’t tied to lofty AI targets.

Plus, NFLX’s at-home leisure mannequin isn’t simply disrupted by AI, and it’s one of many final small luxuries that folks reduce on.

Picture Supply: Zacks Funding Analysis

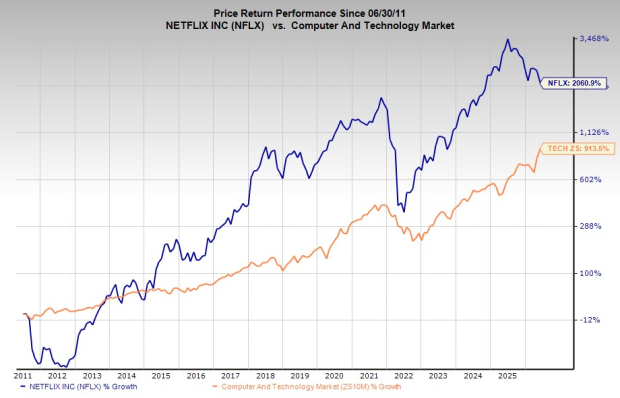

NFLX inventory has skyrocketed ~20,700% previously 20 years and 750% previously decade, to blow away tech throughout each durations.

But, its current fall, coupled with its sturdy earnings progress outlook, has it buying and selling at a 60% low cost to its highs and 15% beneath Tech at 22.0X ahead 12-month earnings. Netflix is buying and selling at a few of its most oversold RSI ranges within the final 10 years and making an attempt to carry its floor at a key 2024 breakout vary.

NFLX’s common Zacks worth goal marks 42% upside from its present ranges, and it must soar practically 65% to return to its all-time highs.

Picture Supply: Zacks Funding Analysis

Netflix’s stability sheet is robust, enormously increasing its shareholders’ fairness previously five-plus years. It is usually now churning out sturdy free money circulate progress, boosted by its capability to lift costs, streamline operations, and extra. And it isn’t caught up within the AI arms race that’s beginning to drain the Magazine 7’s money reserves.

NFLX formally dropped out of the bidding struggle to purchase Warner Bros. Discovery. The transfer will transform a win in the long term because it preserved its core enterprise mannequin and stability sheet. Netflix stated it crossed the 325 million paid memberships milestone within the closing quarter of 2025, up from 302 million in 2024.

Picture Supply: Zacks Funding Analysis

The streaming TV large Netflix rolled out a lower-cost, ad-supported subscription plan within the fall of 2022. The ad-based tier has gained a ton of momentum since then, serving to it compete in a extremely aggressive streaming market.

On high of that, Netflix’s enlargement into dwell sports activities (offers with the NFL, WWE, and far more), actuality TV, podcasts, and extra has helped it retain and appeal to subscribers. It’s even rolling out online game content material.

Picture Supply: Zacks Funding Analysis

The corporate is projected to develop its income by 14% in 2026 and 12% subsequent 12 months to succeed in $57.47 billion. This YoY progress is roughly according to its 12.7% common gross sales enlargement within the trailing 5 years.

NFLX is projected to develop its earnings by 42% in 2026 and seven% in FY27, following 28% progress final 12 months and 65% in 2024.

Radical New Know-how Might Hand Buyers Enormous Features

Quantum Computing is the following technological revolution, and it might be much more superior than AI.

Whereas some believed the know-how was years away, it’s already current and shifting quick. Massive hyperscalers, similar to Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to combine quantum computing into their infrastructure.

Senior Inventory Strategist Kevin Cook dinner reveals 7 fastidiously chosen shares poised to dominate the quantum computing panorama in his report, Past AI: The Quantum Leap in Computing Energy.

Kevin was among the many early consultants who acknowledged NVIDIA’s monumental potential again in 2016. Now, he has keyed in on what might be “the following massive factor” in quantum computing supremacy. Immediately, you may have a uncommon likelihood to place your portfolio on the forefront of this chance.

See Prime Quantum Shares Now >>

Netflix, Inc. (NFLX) : Free Inventory Evaluation Report

iShares Semiconductor ETF (SOXX): ETF Analysis Experiences

Uber Applied sciences, Inc. (UBER) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.