Reporting outcomes for its fiscal second quarter yesterday night, Broadcom AVGO) delivered one other blowout quarter, however shares have fallen as a lot as 15% in Thursday morning’s buying and selling session.

The post-earnings sell-off might have traders questioning if this pullback presents a beautiful shopping for alternative or whether or not expectations for the substitute intelligence (AI) chief have grow to be too elevated.

That mentioned, let’s study Broadcom’s newest Q2 outcomes and see if the latest dip deserves a more in-depth look, with AVGO nonetheless sitting on exhilarating positive aspects of +400% within the final three years.

Picture Supply: Zacks Funding Analysis

Broadcom Posts File Q2 Outcomes

Broadcom posted report Q2 income of $22.18 billion, representing a 48% 12 months over 12 months improve from $15 billion within the prior 12 months quarter and edging estimates of $22.03 billion.

AI remained the first progress engine, fueling Broadcom’s semiconductor options section, which generated $15 billion in income, whereas infrastructure software program income reached roughly $7.2 billion.

On the underside line, adjusted earnings climbed 54% to a quarterly peak of $2.44 per share versus Q2 EPS of $1.58 a 12 months in the past and surpassed Wall Road’s expectations of $2.40.

Picture Supply: Zacks Funding Analysis

AI Demand Continues to Gas Explosive Development

Notably, Broadcom’s AI semiconductor income surged 143% YoY to $10.8 billion, reflecting robust demand from hyperscale cloud suppliers and enormous AI mannequin builders. This comes amid excessive demand for Broadcom’s customized AI accelerators, networking options, and connectivity merchandise that assist next-generation AI infrastructure.

Positioning the corporate as one of many largest beneficiaries of the continued AI infrastructure buildout, Broadcom’s buyer base contains a number of the largest AI spenders on this planet, together with Alphabet GOOGL), Meta Platforms META), OpenAI, and Anthropic.

Moreover, administration supplied a extremely optimistic outlook for the present quarter, anticipating Q3 semiconductor income to achieve roughly $16 billion, which might signify greater than 200% progress from the prior 12 months interval.

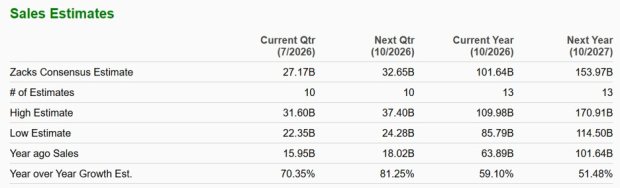

General, Broadcom tasks Q3 income at $29.4 billion, which might replicate an 84% YoY improve and got here in forward of Wall Road’s forecast of $27.17 billion, or 70% progress (Present Qtr under).

Picture Supply: Zacks Funding Analysis

The Bull Case for Shopping for the Dip

1. AI Development Stays Distinctive

Broadcom continues to submit a number of the quickest AI-related progress charges within the semiconductor business. Triple-digit AI income progress demonstrates that demand stays removed from saturated.

2. Sturdy Buyer Relationships

The corporate maintains deep partnerships with main hyperscalers and AI builders, creating long-term income visibility and serving to safe future customized silicon tasks.

3. Diversified Enterprise Mannequin

Not like many AI-focused chip firms, Broadcom advantages from each semiconductor and software program income streams. Its infrastructure software program section gives recurring money stream that may assist cushion cyclical fluctuations in {hardware} demand.

Causes Traders Could Wish to Keep Affected person

Whereas Broadcom’s fundamentals stay compelling, traders must also contemplate a number of dangers.

1. The inventory had already appreciated considerably earlier than its Q2 report, leaving little room for disappointment. Even after the pullback, Broadcom’s valuation stays elevated relative to historic norms, with AVGO buying and selling at practically 50X ahead earnings in comparison with its decade-long median of 18X.

2. Moreover, a lot of Broadcom’s future progress story is determined by continued AI spending by a comparatively concentrated group of enormous prospects. Any slowdown in hyperscaler AI investments may strain progress expectations.

3. There are additionally questions surrounding margin sustainability as AI {hardware} turns into a bigger share of the enterprise combine. Holding this in thoughts, traders might must see continued execution earlier than the inventory regains extended momentum.

Picture Supply: Zacks Funding Analysis

Abstract & Conclusion

Broadcom’s Q2 outcomes have been objectively spectacular. Income jumped 48%, AI semiconductor income soared 143%, earnings topped expectations, and administration guided for one more quarter of explosive progress forward.

Nonetheless, the market’s response serves as a reminder that distinctive firms can nonetheless be susceptible when expectations grow to be terribly excessive. Whereas Broadcom stays one of many premier AI infrastructure performs, traders might wish to stay disciplined relating to valuation and near-term volatility.

For now, Broadcom inventory carries a Zacks Rank #3 (Maintain).

Past Nvidia: AI’s Second Wave Is Right here

The AI revolution has already minted millionaires. However the shares everybody is aware of about aren’t prone to preserve delivering the largest earnings. AI’s second wave is shifting from infrastructure to implementation and these firms are on the forefront of this transition, positioned to grow to be what Amazon and Google have been to the web period.

Broadcom Inc. (AVGO) : Free Inventory Evaluation Report

Alphabet Inc. (GOOGL) : Free Inventory Evaluation Report

Meta Platforms, Inc. (META) : Free Inventory Evaluation Report

This text initially printed on Zacks Funding Analysis (zacks.com).

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially replicate these of Nasdaq, Inc.